$275 Billion in Student Aid — So Why Are Families Still Struggling to Understand College Costs?

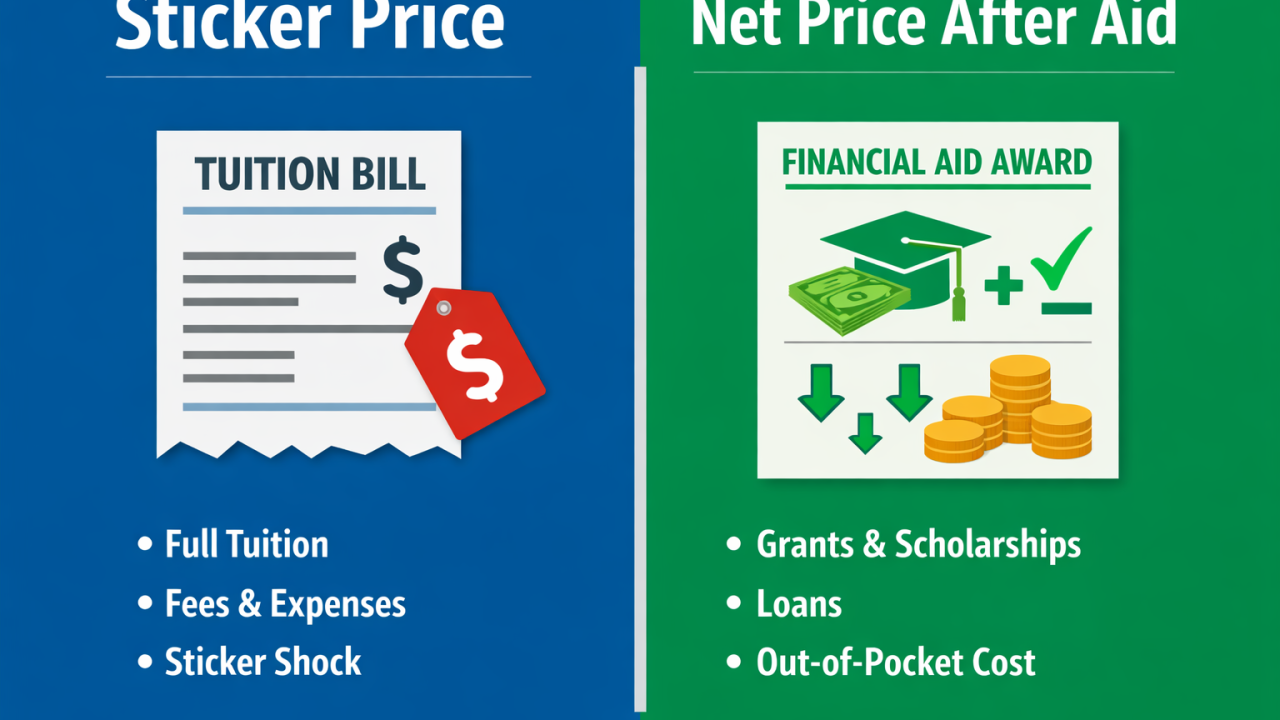

The headline sounds reassuring. In 2025, students in the United States received $275.1 billion in student aid. So why do so many families still feel uncertain — even anxious — about paying for college? Here’s what the data actually tells us. The $275 billion in student aid figure includes grants, loans, tax credits, and work-study earnings. It is a national total — not a guarantee of affordability for any individual student. For families, what truly matters is net price after grants and how much of an aid package must be repaid. Grant aid totaled about $173.7 billion, and both federal and institutional grants increased. Colleges are competing more aggressively for enrollment and using aid strategically to shape incoming classes. That is good news in some respects. But eligibility is uneven. Federal grants are largely limited to U.S. citizens and eligible residents. International students often depend on institutional merit awards. Even with recent increases, need-based grants have not fully regained their historical purchasing power. Borrowing has also begun to rise again after several years of decline. Total loans reached $102.6 billion, with graduate borrowing increasing. Loans remain central to the U.S. funding model. That means repayment literacy matters just as much as admission success. There is one encouraging sign: net tuition at public and private nonprofit institutions has moderated compared to its peak a decade ago. But tuition is only one part of total cost. Housing, insurance, travel, and living expenses continue to rise. Families should calculate the cost of a degree — not just the first-year bill. For global families comparing options, the U.S. model is structurally different from other systems. Nordic countries emphasize state-subsidized tuition. The UK operates under income-contingent repayment. Australia uses deferred contribution schemes. The U.S. blends federal grants, institutional discounting, and loans. Each distributes risk differently. Understanding those differences is essential before making a decision. One of the most common mistakes I see is treating financial aid as something to consider after admission. In reality, financial strategy should be integrated into academic strategy from the start. Institutional selection affects aid probability. Academic positioning influences merit awards. Timing and documentation affect eligibility. Families who plan 18–24 months in advance consistently make stronger financial decisions. The 2025 Trends in Student Aid report does not signal crisis. It signals complexity. And complexity demands clarity. If we are serious about expanding access to higher education, we must treat affordability planning with the same rigor as academic preparation. Admission without a sustainable financial strategy is not opportunity — it is risk. The real question for schools, counselors, and families is this: Are we preparing students not just to get in, but to graduate without avoidable financial strain? Thoughtful planning turns complexity into confidence. And confidence is what families need most in today’s admissions landscape. #CollegeAdmissions #HigherEducation #FinancialAid #CollegeCounseling #EducationStrategy #GlobalEducation #UniversityAdmissions #ParentGuidance #StudentSuccess